下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:高盛

目标价:11.75港币

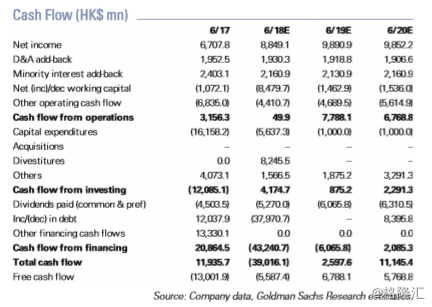

NWD reported better-than-expected underlying profit on accelerated China sales bookings. The 8% increase in interim DPS surprised to the upside, and management expects a further uptick upon full contributions from Victoria Dockside. China land banking was also a focus. After securing a new deal in Shenzhen, management expects to continue a relatively fast pace, with a c.HK$20 bn capex budgeted. Raising 12-month PT to HK$11 .75 (from HK$11 .40). Maintain Neutral.

Results highlights

1H FY18 underlying profit was HK$4.2 bn, vs. our HK$3.7 bn inn 1HFY17 (excluding one-offs), largely due to stronger-than-expected China development property (DP) sales, partly driven by faster-than-expected property sales bookings in China amid higher gross profit margins of 46%, up 10pp yoy. The higher sales resulted in China DP segment profit of HK$4.0 bn, or 49% of the group’s total. BVPS was up 7% hoh to HK$20.33, partly helped by an HK$7 bnn positive revaluation in the HK office segment. Interim DPS surprised, rising 8% yoy to HK¢14. Managementn explained the increase was due to its plan to ramp up cash returns amid the phased completions of Victoria Dockside (only a partial contribution from the office segment during the period).

Hong Kong

NWD achieved HK$7 .1 bn of contracted sales for the fiscal yearn to February, or 71% of the HK$10 bn full-year target. The company’s early adoption of HKFRS 15 did not lead to an significant difference in booked profit as guided by