下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:国泰君安

评级:中性

目标价:35港币

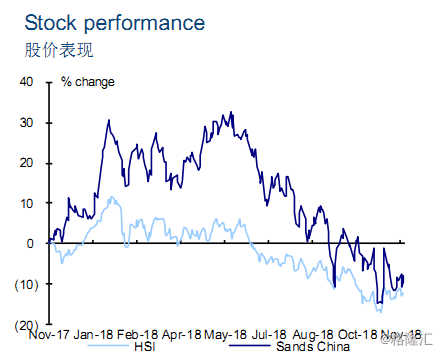

Sands China (the "Company")'s 3Q18 adjusted property EBITDA increased 15.8% yoy to US$754 mn, in line with market expectations. Company-wide overall VIP win rate was 3.27%, much higher than the 2.90% experienced in 3Q17 but lower than the 3.47% in 2Q18. Assuming a company-wide overall 3.15% VIP win rate, normalized adjusted EBITDA would have increased by 11.5% yoy to US$745 mn, in line with Bloomberg consensus forecast but less than our previous expectation. The Company's

total market share increased by 1.2 ppt yoy and 0.3 ppt qoq in 3Q18.