下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:麦格理

评级:买入

目标价:14.56港元

Key points

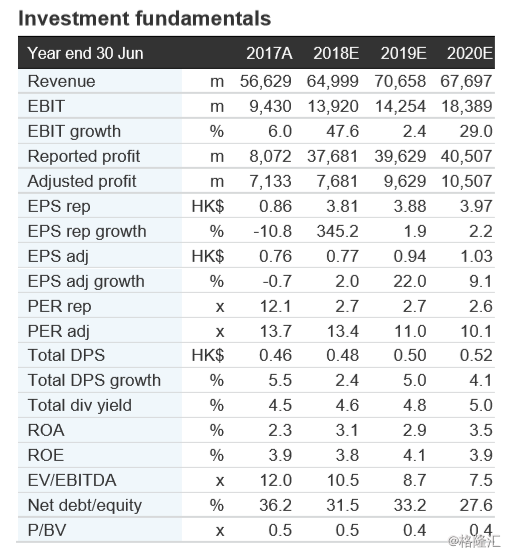

The company will report FY18 after market close. We expect core profit of HK$7.7bn, up 7.7% YoY.

Property sales should be sustained in FY19 and we project 25% earnings growth for FY19 and 9% for FY20.

K11 MUSEA and K11 ARTUS should open in 2019, boosting NAV.

Price catalyst

12-month price target: HK$14.56 based on a Sum of Parts methodology.

Catalyst: more pre-leasing progress of K11 MUSEA. Action and recommendation

Stock is trading at 0.5 PB and 50% discount to NAV. Reiterate Outperform.