下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:信达证券

评级:卖出

目标价:3.03港元

Loss expected in 1H18 due to RMB depreciation, components shortage and slow product optimization; Earnings visibility still low

Q Tech issued an updated profit warning alert after market close last Friday (Jul 13) which expects a net loss ~RMB50 mn in 1H18 vs. profit before tax (PBT) in 1H18 would drop ≧50% Yoy mentioned in the announcement on May 10. Management attributed that to i) ~3.8% RMB depreciation during in May and June; ii) slower CCM sales dragged by raw materials and components shortage and iii) slow product optimization in both CCM (mainly supplying low margin 2MP CCM to Huawei) and fingerprint recognition modules. In addition, we continue to believe the i) adoption of more aggressive pricing strategy; ii) lower than expected CCM product yield dragged by wider adoption of integrated lens set (MOC) which Q Tech is still on the learning curve; iii) lower than expected utilization rate due to weakened market demand while Q Tech has expanded their capacity by >50%; Q Tech’s total CCM shipped though accelerated to 22.4% Yoy/27.4% QoQ to 58.9mn and brought 1H18 total shipment to 102.8mn (+23.6% Yoy, accounted for 54% of our estimates. The CCM growth was well ahead of our FY18E forecast (190mn shipment, +10%). However, the ≧10MP shipment only accounted for 38.0%/36.2% of the total shipment in May and June (vs. record low at 32.3% in Jun 2017), while ≦8MP CCM shipment made up ~60% of total in 1H18 vs. 44.5% in 4Q17 after tapping into Huawei’s supply chain (mainly supplying low margin 2MP CCM). Though Q Tech is reported to be the sole supplier for OPPO Find X’s 25M P O-face recognition front camera module, while also being the 2nd tier supplier for vivo NEX’s 8MP front camera module, we expect the contribution to Q-tech would be minimal. We also noted that Q tech is reported to have already shipped 3D structured light camera module samples to Huawei and target to be one of the suppliers (other suppliers include Sunny Optical and O-film)for the rumoured Mate 20 (expected to be unveiled in late 2018).

On-screen FPC plays the majority in FY18E with ASP pressure

In 1H18, Q-Tech shipped 45.1mn pieces of FPC (+31.6% Yoy) which accounted for 46.6% of our FY18E estimates (volume +20% in FY18E) and vs. 42.50% in 1H17. Q Tech has started to ship small amount of optical/under screen FPC to clients in 2Q18, however, we expect FPC would make up the majority of FY18E shipment. We noticed that the adoption of optical/under screen FPC by Chinese brands’ flagships has been gradual (adopted in Vivo X20 plus UD, X21 UD, NEX flagship, Huawei Mate RS Porsche Design, Xiaomi Mi 6, Mi 8 Explorer Edition and OPPO’s Find X) and due to lack of product upgrades for on screen FPCs, we still expect ASP would still face downside pressure in FY18E/19E. Slash FY18E-20E mainly on lower GM assumption; Maintain Sell

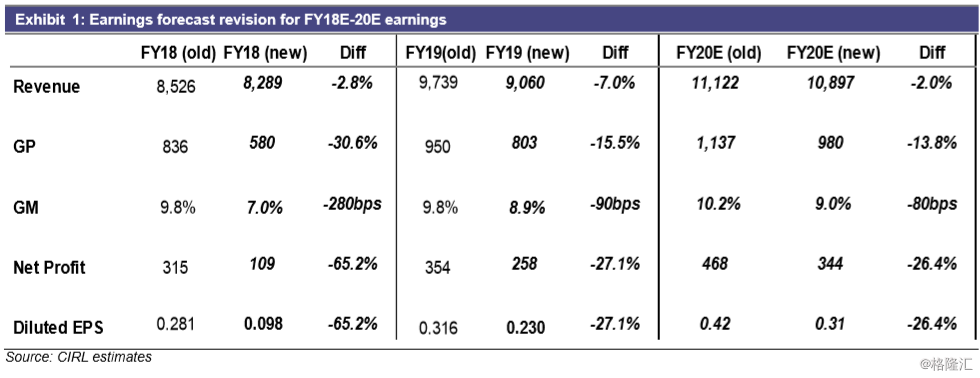

We further cut Q-tech’s FY18E/FY19E/20E diluted EPS by 65.2%/27.1%/26.4% earnings, by factoring in lower sales forecast and GM assumption, we expect Q-tech’s FY17-20E diluted EPS to grow -7.6% CAGR (vs. ~83% CAGR in FY15-FY17). We slashed Q Tech’s TP from HK$4.26 to HK$3.03 (which implies FY19E 11.1x PE) and 45% discount (same as in our last update in May 2018) to leading players including Sunny Optical (2382.HK), O-Film (002456 CH) and LG Innotek (011070 KS) to leading players’ average PE at 20.2x. Given its unattractive valuation and in view of blurred visibility on Q Tech’s CCM business, we believe this profit warning update further shreds investors’ confidence in Q Tech, we reiterate Q-tech’s Sell rating.