下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:招商证券

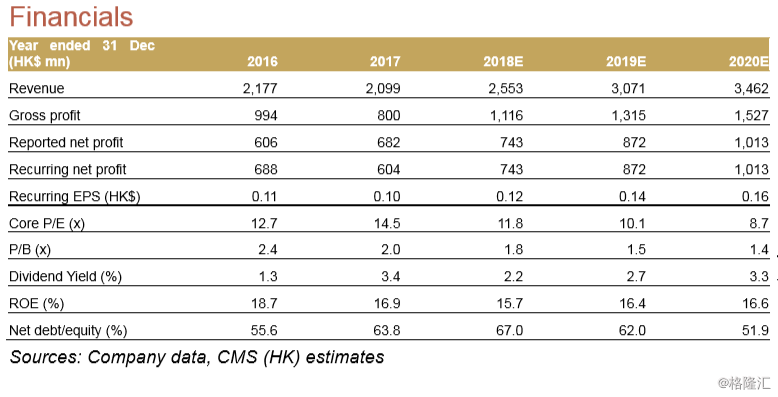

Inline FY17 results

CTEG’s FY17 core profit dropped 12% YoY to HK$604mn, largely in line with our estimates, but 6% below consensus. The profit was mainly dragged by: 1) the loss status of its newly commenced Fumian project given the slow ramp-up; and 2) lower-than-expected utilisation of sludge and general solid waste treatment (4% YoY revenue growth) and hazardous waste treatment business (revenue dropped 8% YoY) due to the facilities upgrades and maintenance.

Guiding a positive 2018

CTEG is speeding up the development of Fumian Project Phase I & II and Bobai Project Phase I & II. With the commencement of these projects in 2018-19, together with more tenders received for sludge and general solid waste treatment and hazardous waste treatment business starting from Dec 17, mgmt. guides a 30% YoY growth in NP in 2018.

Maintain NEUTRAL and slightly adjust our TP to HK$1.52

We basically maintained our forecasts with only very minor adjustment due to the announced results. Accordingly, we lower our DCF-based TP by a slight 2% to HK$1.52. While we see limited downside risk for CTEG at the current valuation level (2018E P/E of 11.8 with 20% recurring EPS CAGR in 2017-19E), the auditor’s qualified opinion on HK$62mn of sludge and solid waste treatment service revenue might affect investors’ confidence on the co.’s execution abilities. Despite the affected amount only accounted for less than 3% of the total turnover in 2017 and the co. promised to have a better book keeping for new customers going forward, we believe it takes some time for the co. to regain investors’ confidence. We maintain NEUTRAL.