下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:交银国际

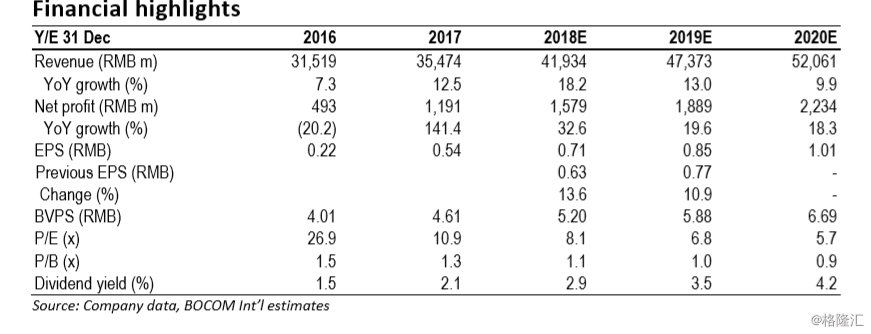

Mixed results. Zhengtong Auto’s FY17 net profit surged 141.4% YoY, largely in line with pre-alert, and 2% higher than market expectations. The major beat came from GPM improvement, from 8.7% in FY16 to 10.6% in FY17, driven by new car sales margin (4.9% in FY17 vs 2.9% in FY16). Major misses came from lower dividend payout ratio and high net gearing ratio. The payout ratio decreased from 40.1% in FY16 to 23.6% in FY17. Net gearing ratio climbed from 97.6% in FY16 to 128.6% in FY17.

26 new dealership stores in FY17 to generate volume growth in FY18. In FY17, Zhengtong recorded new car sales volume of 109,016 units, up 12.5% YoY, underpinned by 17.7% growth of luxury and ultra-luxury brands. The company opened 16 new dealership stores and added 10 more through strategic cooperation in 2017. We expect these new dealership stores to translate into sales volume growth in FY18. The company has 16 authorized luxury & ultra-luxury dealership stores to be opened from FY18 onward.

Interest income from financial services on track. Auto finance revenue rose 31% YoY to RMB522m. Segment operating profit surged 71% YoY to RMB378m, which was 10% higher than management guidance. Bad debt ratio was still very low at 0.27% in FY17. We believe the previous share placements and auto financing penetration growth will support its financing business growth.

Stretched B/S is an overhang, but growth outlook intact. We revise up FY18/19 earnings forecasts by 13.6%/10.9% to reflect higher new car sales volume growth and auto finance business growth. We maintain our Buy rating, but lower our TP from HK$9.50 to HK$7.95, based on 9.7x FY18E P/E (previously 13x), mainly due to its stretched B/S and lower dividend payout ratio ahead. Fast auto finance growth at the expense of B/S quality could be an overhang on valuation, in our view.