下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:德意志银行

评级:持有

目标价:5.7港元

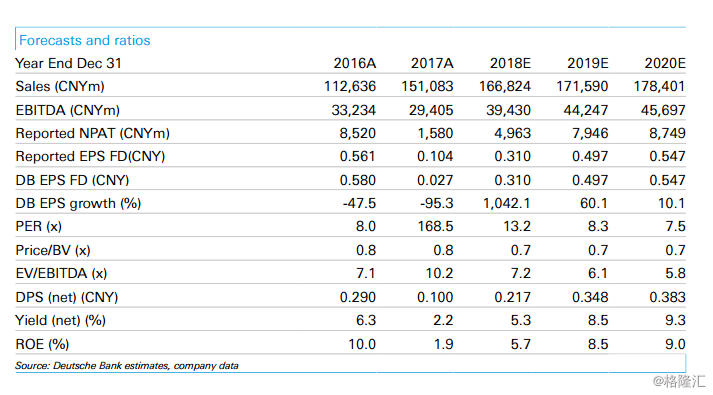

Hua neng Power reported weak 3Q18 results with a net loss of Rmb 140mn, which is unexpected as the 8% yoy output growth and 1% yoy higher tariffs were not enough to offset the rising costs. Earnings are mainly dragged by a 11% yoy increase in cost of operations (we estimate a 7% yoy higher unit fuel cost in 3Q18),12% yoy higher financial cost, and Rmb 229mn loss in investment income. Going into 4Q, we see increasing fuel cost pressure as the QHD coal prices are still on the rise. We think Hua neng is trading at unattractive 2019E valuations (0.7x P/B)and the slower-than-expected earnings recovery is also a negative on the dividend outlook. Hold.