下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

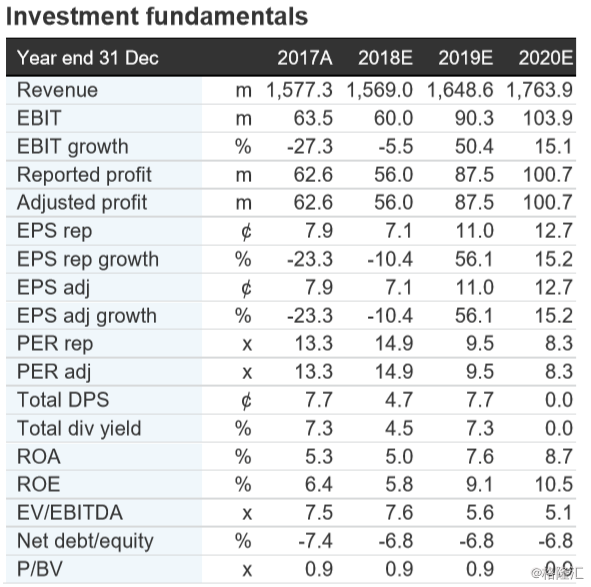

机构:麦格理

评级:买入

目标价:13.00港元

Key points

Shipment volume growth maintained while ASP continued to drop.

Redundancy cost to reach ~US$20m for FY18 and FY19;

potential idle asset disposal.

Financial position capable to support dividend policy.

Earnings and target price revision

We lower our net profit by 11.4% and 1.1% for FY18E/19E. TP remains unchanged at HK$13/sh. Price catalyst

12-month price target: HK$13.00 based on a PER methodology.

Catalyst: 3Q18 operation result

Action and recommendation

Maintain Outperform.