下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:兴业证券

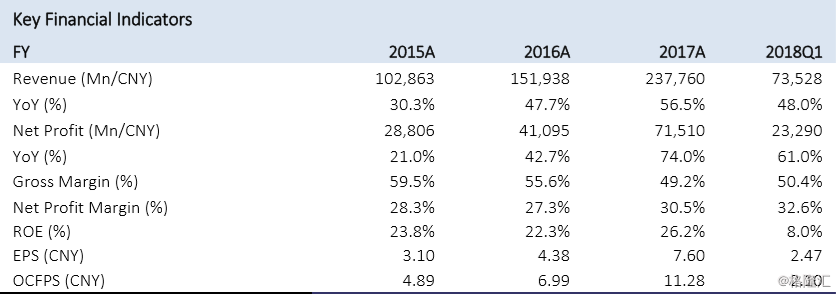

Company Profile Tencent Holdings Limited is an investment holding company principally involved in the provision of value-added services (VAS) and online advertising services. The Company operates through three main segments. The VAS segment is mainly involved in provision of online/mobile games, community value-added services and applications across various Internet and mobile platforms. The Online Advertising segment is mainly engaged in display based and performance based advertisements. The Others segment is mainly involved in provision of payment related services, cloud services and other services. (Source: Reuters) Comments The company’s gaming business registered strong and market-beating rebound. Tencent recorded 68% yoy uptick in the sales revenue of its gaming business. Driven by DAU’s and ARPU’s yoy hike of ‘Glory of the King’, the average DAU of ‘QQ-Racing for Speed’ surged to 7 times of the data on PC-side, suggesting its user base of PC-games is draining as the outflow speed being higher than that of inflow. However, Tencent has kept stable revenue growth of its PC-games under such background.

Impacted by growing subscriptions of its paid-music website and of exclusive contents in its videostreaming platform, company’s revenue from social networking service ramped up 47% yoy and 16% QoQ. Video-streaming sector contributed the most momentum, with daily views, platform revenues, subscription revenues and advertising revenues surging respectively 60% yoy, 75% yoy, 85% yoy and 64% yoy. Tencent recorded aggressive expansion of online advertising business, underscoring its advantages in information-stream advertising. Sales of the company’s online-advertising business posted a 55% leap from previous year to CNY 10.7 bn. Social-networking counted as one of the strongest drivers by reporting a sales growth of 69% yoy.

Growth of e-payment- and cloud-service business has doubled: the business expanded 111% yoy, with the weight of its revenue among the company’s total hiking from 18.23% in 2017 to 21.71% in Q118 and with its gross margin hiking 21.87% in 2017 to 25.39% in Q118. We attribute the growth to high spreading speed of e-payment and of Tencent’s small cellphone-programs attached to WeChat. At the same time, Tencent enjoys rapid revenue growth of cloud-services, benefiting by rich experience in video-cloud and gaming-cloud services.

Beefing up investment to seize potential trend of future. Tencent plowed CNY 21.1 bn to its affiliated companies during Q118 (increasing the size of its available-for-sale financial assets by CNY 54.88 bn) , which is over 2 times of Alibaba’s and over three times of Baidu’s. We are positive about stable expansion of China’s gaming industry and we expect e-payment and digital businesses to become new growth driver for Tencent. Potential risks: 1) Advertising business may register weaker-than-expected gross margin. 2) Growth of company’s gaming-business may decline. 3) Unexpected and unfavorable policy-control.