下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:中金公司

评级:买入

目标价:40.31 港元

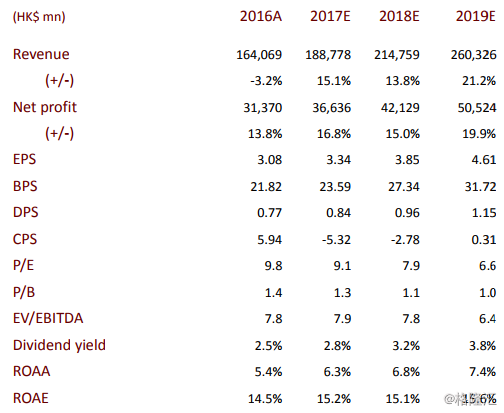

Be well prepared for a bottoming-out of sales growth in 2018. Sales of HK$300bn (YoY +29%) should be easily generated from sale able resources as abundant as HK$450–500bn, after a fruitful 2017 with17.4mn m2of land replenishment and 19mn m2of GFA new starts.Strong growth in January (est. >20% YoY) despite a high base should trigger an upward consensus revision, and the growth will further improve in 2H18e due to a lower base. Therefore, we think COLI will not fall behind peers any more in 2018.

Lucrative margins to uplift earnings delivery. Booked GPM is estimated to be 30.2%/30.1%/30.7% in FY17/18/19, thanks to sales GPM being consistently above 30% in 2016/17.

Strong balance sheet to lay a firm foundation for scale expansion.Net gearing ratio was well capped below 40% at end-FY17 (21.2% atend-3Q17). Combined with ambitious sales in 2018e, COLI should be comfortable with mildly quickening expansion. Its sector-leading capacity for fund raising―average financing cost as low as 4.2% in1H17―will secure the land purchases.

Valuation and recommendation

Maintain FY17e core NP of HK$36.6bn (YoY +17%); trim FY18e coreNP slightly by 4.6% to HK$42.1bn (YoY +15%) and introduce FY19e ofHK$50.5bn (YoY +20%) for delivery adjustment. Reaffirm as sector toppick and hold TP at HK$40.31 (33% upside). We regard COLI as aquality laggard with visible & better-than-expected sales,defensiveness, and more importantly, an attractive valuation. COLItrades at 7.9x FY18e and 6.6x FY19e P/E (below its average of the pastseven years), on par with small caps like Agile and CIFI.

Risks

2018e sales fall short of expectations.